According to the Canadian Federation of Independent Business, over 75% of Canadian business owners plan to exit their business within the next decade. As you prepare for this transition, understanding the options available to you during the sale of your business is crucial to ensure a harmonious and tax-efficient transfer of assets. Among these options, transfers to employee ownership trusts offer a unique solution that can help to support the long-term stability of your business and create potential tax savings.

Starting January 1, 2024, business owners can access significant tax benefits when selling a qualifying business to an employee ownership trust (‘EOT’) pursuant to a transaction (an ‘EOT Transaction’) that constitutes a qualifying business transfer (‘QBT’). Among other benefits, eligible vendors are entitled to receive a shared pool of up to $10 million in capital gains deductions (the ‘EOT Deduction’).

This article will provide an overview of the eligibility requirements for the $10 million EOT Deduction and an outline of the various benefits of EOT Transactions. We have also included diagrams for a sample pre-closing structure illustrating where an EOT Transaction could be implemented and a sample post-closing structure illustrating how the EOT Transaction could be funded.

What is an Employee Ownership Trust?

In a subsequent article which will be titled ‘Employee Ownership Trusts: A Guide to Structuring and Settlement,’ we will discuss the employee ownership trust qualification requirements, trust property distribution restrictions, and what is needed for a transaction to be considered a QBT. Once published, it will be available on our website.

For the purposes of this article, an employee ownership trust can be understood as an irrevocable trust which is resident in Canada and meets certain conditions concerning beneficiaries, trustees, trust distributions, trust property, and fundamental decisions. Unlike traditional ownership models, where shares are owned by individual shareholders, an employee ownership trust model allows the employees of a business to benefit from the growth and success of the company as beneficiaries of the employee ownership trust which is the controlling shareholder.

Employee ownership trusts are a particularly effective solution for business owners looking to transition ownership in a way that preserves the company legacy and enables the owners to take advantage of significant tax savings, making it an appealing option for both owners and employees.

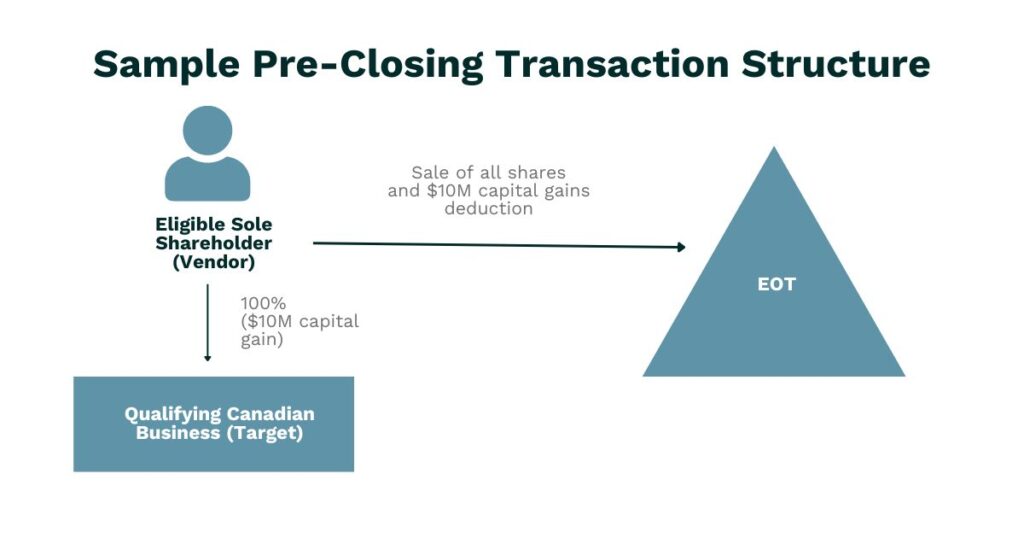

Employee Ownership Trust Sample Transaction Structure with a $10 Million EOT Deduction

To demonstrate where an EOT Transaction may be beneficial, illustrated below is a simplified example of a pre-closing transaction structure that highlights the benefit of the EOT Deduction. In this example, a Canadian controlled private corporation (‘CCPC’) is entirely owned by an individual whose shares represent $10 million of unrealized capital gains.

If these shares were sold to a third party, the individual would realize a $10 million capital gain which would be taxable at their marginal tax rate. This would apply unless an applicable capital gains exemption or deduction was used, such as the lifetime capital gains exemption – currently available for up to only $1.25 million. Instead, if the shares are sold pursuant to an EOT Transaction, as pictured below, the $10 million capital gain would be offset by the $10 million EOT Deduction, effectively eliminating the individual’s capital gains tax liability. For an Ontario resident with a marginal tax rate of 53.53%, this could result in a tax saving of more than $3.5 million in certain circumstances.

Employee Ownership Trust Deduction Eligibility Requirements for Business Owners

Business owners, whether partners in a partnership, shareholders of a corporation, or the sole proprietor of an unincorporated business, may be eligible to complete an EOT Transaction. Generally, vendors who want to claim the EOT Deduction will need to sell their shares of a CCPC to an employee ownership trust. If the vendors do not have an existing CCPC, they may be able to incorporate their business. It must be an active business in which the vendors have been actively involved and have held an ownership interest for at least two years.

More specifically, the EOT Deduction should be available if the business meets the following key requirements:

- Transaction Deadline: The shares in the CCPC must be sold to an employee ownership trust on or before December 31, 2026.

- Active Involvement by the Owner: The vendor (or their spouse or common-law partner) must have been actively engaged in the business on a regular and continuous basis for a 24-month period at any time before completing the EOT Transaction.

- Active Business: During the entirety of the 24-month period before the sale, more than 50% of the fair market value of the shares must be derived from assets used principally in an active business.

- Canadian Resident Owners: The controlling business owners must be residents of Canada.

- Canadian Resident Employees: 75% or more of the employees are residents of Canada.

- Non-Publicly Traded: The business cannot be a corporation listed on a designated stock exchange.

- De-professionalization: If the CCPC is a professional corporation, it must be de-professionalized before the EOT Transaction.

- Existing Business: During the entirety of the 24-month period before the sale, the shares of the CCPC must not have been owned by anyone other than the vendor or a related person or partnership.

Additionally, to be eligible for the EOT Deduction, the transaction must meet the necessary requirements for it to constitute a QBT. We will discuss this further in our second article on the topic.

Benefits of Employee Ownership Trusts

The primary benefit of an EOT Transaction is the ability to claim the $10 million EOT Deduction. However, there are also several other benefits. Specifically, to facilitate such transactions, employee ownership trusts benefit from the following:

- 21-Year Rule Exemption: Unlike other trusts, an employee ownership trust is exempt from having a deemed disposition of its assets every 21 years.

- Shareholder Loan Income Inclusion Exemption: Unlike other shareholders, an employee ownership trust is not required to include in its income a low-interest or non-interest-bearing loan that it receives from a qualifying business it acquired pursuant to an EOT Transaction if the loan was solely provided to finance the transaction. Arrangements must also be made for the loan to be repaid within 15 years.

- Extended Capital Gains Reserve: If an EOT Transaction triggers capital gains exceeding available deductions and sale proceeds are paid over several years, the vendors can claim the capital gains reserve. This allows them to spread out their capital gains tax liability over a period of up to ten years instead of the generally available period of only five years. The extended time period for claiming the capital gains reserve incentivizes longer-term vendor take-back financing periods which eases short-term payment obligations and facilitates cash flow management for the employee ownership trust.

Other Employee Ownership Trust Transaction Considerations

Before implementing an EOT Transaction, consider the following:

- Taxation: Employee ownership trusts are generally taxed like other personal trusts, with undistributed income taxed at the top personal marginal tax rate. Therefore, an employee ownership trust should be seen as a vehicle for allocating profits to employees within the same year and not for storing large cash reserves.

- Extended Reassessment Period: The reassessment period for the taxation year in which an individual claims the $10M Exemption is extended by an additional three years.

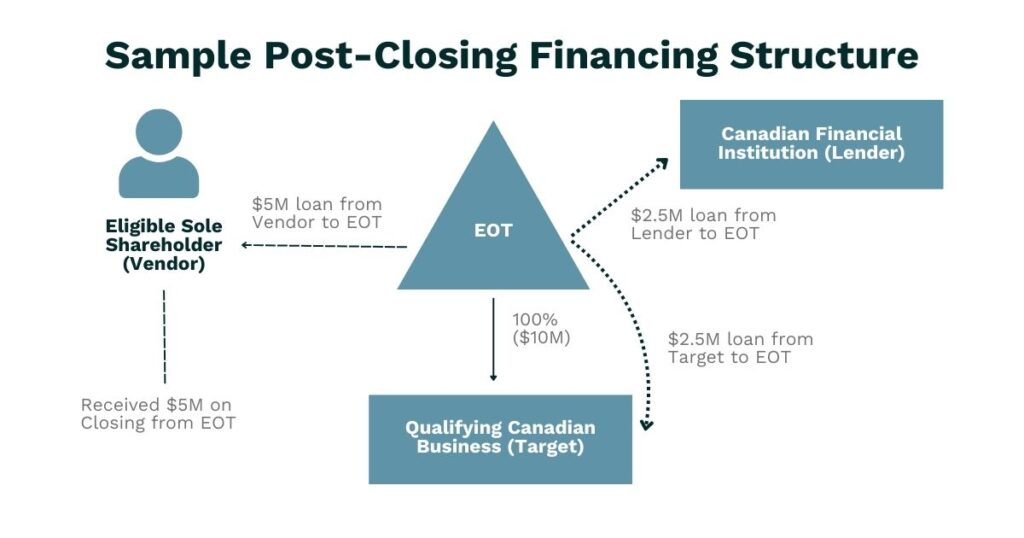

- Financing Challenges: In some circumstances, securing third-party financing for a newly established employee ownership trust can be challenging. As a result, complex funding structures, such as those involving vendor-take-back financing, a partial loan from the target, or a partial loan from a financial institution, may be necessary.

For example, and as illustrated below, in a $10 million transaction, a simplified post-closing structure might involve a $5 million vendor-take-back loan, with the remaining $5 million paid in cash at closing by the employee ownership trust from a $2.5 million loan from the target qualifying business and a $2.5 million loan from a Canadian financial institution.

Conclusion

While there are tax advantages and other benefits, deploying an EOT structure is a complex endeavour. Prior to effecting any relevant transactions, it is important to consult a lawyer who is familiar with the legal framework and capable of implementing a structure optimized for your business.

Reach out to our team of knowledgeable lawyers to discuss how we can assist you in navigating this process effectively.

Authors: Sanjay Kutty, Devon Molloy, James Konopka, and Arianne Carew